The global economy is clearly on the downswing, with the US likely having entered a recession this summer (watch for revisions in GDP and employment data in the coming months). However, as in Sept-Oct 2007, the equity market has bounced from a brief oversold interlude to a new high.

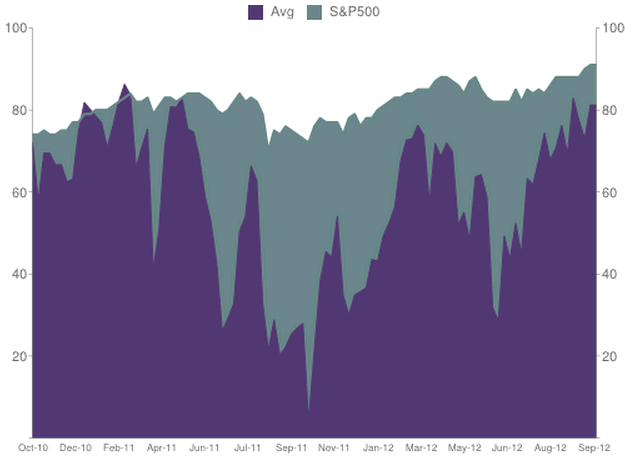

Here is the NAAIM survey. This is a relatively new dataset, but it has proved high-correlated with proven sentiment indicators like DSI and Rydex fund activity). The survey is updated each Thursday with data from Wednesday.

Sentiment has been elevated for a month, which is sufficient for a significant decline, though the likelihood of a setback and the expected magnitude thereof grows with each week that it remains elevated. This, coupled with sideways price action for few weeks (we don’t have this yet) and a declining trend in daily RSI (possibly developing) would virtually lock in the case for an intermediate-term top.

EDIT: To clarify, this is not a screaming short-term sell yet, since the market has had a habit of creaping slightly higher over a few weeks from conditions like this. However, things can reverse at any time, and it is highly likely that any further gains will be quickly erased once the turn comes.

The macro picture of deteriorating economic data bolsters the case that a bull market top is near, so if this is an intermediate-term top it could prove to be the final top prior to a bear market. This cyclical bull is now 3.5 years old. This is long in comparison to the cyclical bulls of the 1910s and 1970s secular bear markets (18-36 months was typical), but short in comparison to the last cyclical bull (spring 2003 – fall 2007, 4.5 years).

Hi Mike,

Would you mind clarifying a bit what you mean by an “Intermediate-term top?”

Does it relate at all to the idea that we are still dealing with Primary 2 up and perhaps finally approaching that top?

Hi Bjorn,

No, the Primary 2 thesis died years ago. We’ve had a whole new bull market here.

An intermediate-term top would be like what we had in early spring 2010, spring-summer 2011, and early spring 2012. Of course, sooner or later one of these will prove to be a final top of the bull market.

BTW, I don’t follow EWI or count waves anymore. I try to keep things much simpler.

Mike,

What strikes me is that EWI uses lots of indicators other than wave theory (as you are well aware) like put/call ratio, advance/decline ratio, sentiment indicators, volitility index, yearly cycles, and on and on.

Those other indicators have, on any number of occasions, seemed to suggest an approaching major top, at least as they were interpreted by EWI, but it has not happened, and 3+ years have passed.

How do you relate to the larger movements these days? You refer to a final top of the bull market. How do you orient yourself so as to anticipate a “final top?”

Some consider a rise of 20% above the last low as a definition of a bull market, or a fall of 20% against the last high as a definition of a bear market. As long as one could successfully navigate such movements money could be made, of course, but this orientation is different from Prechter’s in which he actually anticipates a bear market crash of historic proportions. Do you anticipate such a “historic crash” in which the market could fall as much as 70%, 80%, or even 90%?

Do you use any particular theories, like Dow Theory for example, to orient yourself? You mention keeping things simpler, and I am wondering what you mean by that.

Thanks

I don’t think that such an historic crash is necessary, but I am somewhat anticipating another cyclical bear market within the secular bear that started in 2000, which would be akin to the last two cyclical bears (2000-2003, 2007-2009). It may even be shallower than those – we just can’t tell.

But really, I try not to even think too much about such larger moves, since as we have leared since mid-2009, they are harder to anticipate than intermediate-term moves, which are more predictable using tools such as sentiment (surveys, VIX, Rydex flows) and momentum (RSI is my favorite).

As simply as I can put it, I look for sustained extremes in sentiment (bullish or bearish) that coincide with weakening trends or sideways prices (either at highs or lows), and after such a condition has been sustained for a few weeks, take the contrary side. Right now we have high sentiment that has just barely been sustained long enough to be a contrary indicator. We only have 10 days of price stagnation since QE∞ was announced. If these conditions are sustained a little longer, we will have a strong sell signal.

I don’t employ wave theory or Dow theory or anything like that, because I think that they just confuse the picture and keep you from holding an agnostic view that leaves you open to a wider range of possibilities. I try to avoid dogma, and EWI in particular is crippled by permabear dogma.

The reasons why I think we may experience a bear market soon, which I loosely define as a fall of greater than 30%, are mostly economic (stagnating earnings, faltering employment, and global trade and GDP numbers, etc). Elevated valuations and sustained complacent sentiment also factor in, as does the disconnect betwean US stock prices and those in the rest of the world.

Thank you for your explanation.

A historian friend of mine likes to take a very long-range view of events. He sees current events through the lens of history, which has value in some situations but also creates a certain detachment when it comes to day-to-day decision making. His long-range view might not help someone decide whether it’s a good time to open a restaurant, for example.

The approach you present here would sure have been more useful to me over these last several years than the one I adopted, which was based upon EWI’s assessment. But to be honest, my own inexperience in setting stops played big into my own loses. I was looking long-range and trusting long-range forecasts too much.

I personally find long-range forecasting to be of interest, and that might be an achilles heel when it comes to the investment game. It gets in the way of the flexibility that you are speaking to. I’m going to experiment, on paper for now, with the approach you are describing here to see if I can develop a better sensitivity to the market movement.